PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures lost ground today, while OPEC+ debated output policy for February, amid weakness in US shares - but despite strength in European equities and some weakness in the US dollar. The final December UK CIPS/Markit Manufacturing PMI was a beat at 57.5, but the final December Eurozone Markit Manufacturing PMI saw a surprise downward revision to 55.2. Both still indicated continued expansion in the sector. The FTSE 100 in the UK shot up 1.7% today, while the CAC 40 added 0.7% and the DAX edged up 0.1%. In US economic news, the final Markit Manufacturing PMI for December came in at 57.1, a surprise upward revision from 56.5 in the flash estimate, indicating expansion in the sector accelerated (November was 56.7). Also encouraging, construction spending grew 0.9% in November. While this was just shy of the 1.0% consensus, base effects more than account for that as October spending growth was revised up 0.3pp to 1.6%. Nevertheless, US stock market indexes were dropping as of this writing. The Dow was down 1.6% and both the S&P 500 and Nasdaq had dropped 1.7% lower. The US dollar index, which had hit fresh lows not seen since 2018 earlier in the session, had recovered to a small dip of 0.05% as of this writing. Market participants awaited the OPEC+ February output policy decision; Reuters sources indicated Russia and Kazakhstan were pushing to raise the output ceiling, while other parties sought to keep it steady, and that discussions are to continue tomorrow.

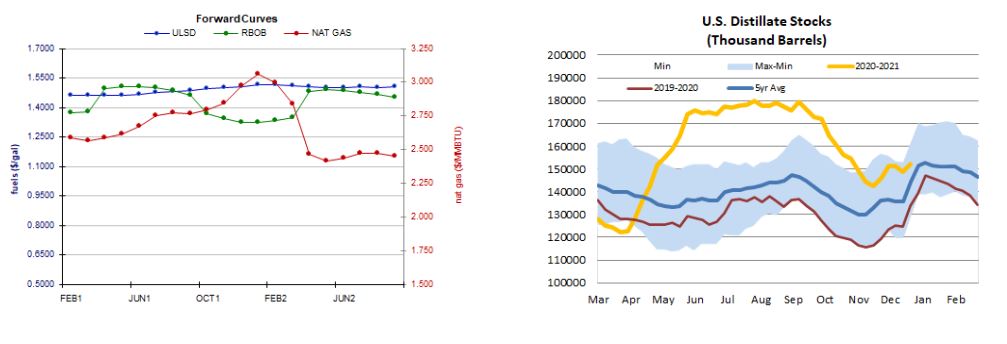

Forward Curves for ULSD RBOB & NAT GAS US DISTILLATE STOCKS

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures gained some ground today as the degree day outlook improved. The Global Forecast System raised its two-week HDD forecast from 381 to 423, below the 462-HDD 30-year average but well above last year's 364 HDDs during the same period. Refinitiv analysts see total US demand of 121.1bcf/d outpacing total US supply of 100.6bcf/d this week by 20.5bcf/d. The market is seen tightening next week as demand rises to 126.1bcf/d while supply slips to 100.1bcf/d, implying larger withdrawals of 26.0bcf/d. Although the HDD outlook overall has improved, above-normal temperatures are still expected on the East Coast over the next 5 days (latest ECMWF forecast) and temperatures in the Midwest are seen well above normal. The 6-10 day outlook sees more mixed temperatures in the Northeast, but still mostly above-normal temperatures in the Midwest, and the 11-15 day outlook sees mostly above-normal temperatures in both regions. In the cash market, Henry Hub prices rose by 3 cents to $2.39/mmBtu, but Transco Zone 6 prices in New York shed one cent to hit $2.31/mmBtu and Algonquin citygate prices fell by 10 cents to $2.38/mmBtu.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures dropped another 1.9% lower in an average-volume session today, but we hit intraday levels not seen since back in March at the highs, making it an outside session (higher high, but also a lower low). We settled near the bottom of the daily range and on the other side of the 9-day ma ($1.4798), which becomes nearby resistance followed by today's $1.5347 high. Next support is expected at the $1.4000 psychological level, followed by $1.3500. Technical indicators remain mixed with bearish slow stochastics and RSI, neutral candlesticks and MACD, while the major averages and ADX point higher. We remain neutral. Similarly, RBOB futures hit a multi-month high of $1.4516 today but came off and settled down 2.6% and below $1.3899 support. This becomes nearby resistance, followed by that $1.4516 high, whereas the 18-day ma ($1.3526) and then $1.3000 are seen offering support. Stochastics and the RSI point lower, but candlesticks and the MACD are neutral, whereas the major averages point higher. We remain on the sidelines here. Trade in WTI was similar, hitting a high of $49.83 but coming off for a 1.9% drop, settling back below the 9-day ma ($47.90) and near the 18-day ma ($47.53). We remain neutral, pending bearish confirmation, seeing 9-day ma and then $49.83 resistance, with $45.27 and then $42.02 support. Finally, NYMEX natural gas futures gapped sharply higher over the weekend, but then came off some, ending 1.7% higher. Slow stochastics and the RSI point higher, and candlesticks are trending higher as well. Major averages are neutral, as is the MACD. We may have missed the boat, but we'll side with the bulls nevertheless, seeing resistance at the 100-day ma ($2.612) and then up at $2.898, with $2.403 and then $2.258 support.