PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex saw see-saw trade near the unchanged mark today, settling higher, with strength in the US dollar likely weighing, whereas gains in US and European shares were supportive. Economic data from Europe were mixed but unsupportive on balance. Eurozone consumer sentiment and German manufacturers orders were a beat, but Eurozone retail sales, the flash Eurozone HICP, and the UK Construction PMI (CIPS/Markit) were all a miss. Nevertheless, European shares strengthened today, with the FTSE 100 up 0.2%, the DAX gaining 0.6%, and the CAC 40 rising 0.7%. In US news, the international trade in goods and services deficit came in at $68.1bn for November, wider than the $66.8bn consensus. On the other hand, weekly jobless claims of 787,000 were lower than consensus at 803,000. US stock market indexes were extending their rally as of this writing, with the Dow up 0.7%, the S&P 500 rallying 1.4%, and the Nasdaq jumping 2.4% higher. Whereas this was supportive for oil prices, a 0.3% rise in the US dollar index was unsupportive.

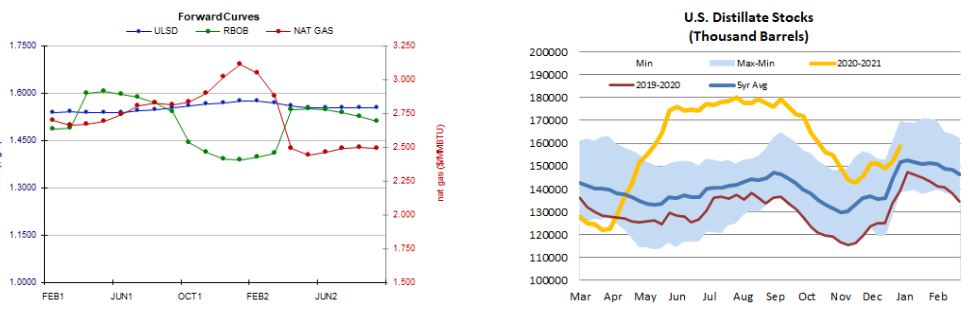

Forward Curves (ULSD | RBOB \ NAT GAS) DISTILLATE STOCKS (US)

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures on NYMEX posted further modest gains today despite an unsupportive weekly storage report from the EIA, and a slight downward revision to the two-week heating degree day outlook. The EIA reported a 130bcf withdrawal from underground storage for the week ended January 1. Although this far exceeded last year's 44bcf withdrawal and also the 101bcf five-year average, it fell short of the 135bcf predicted by analysts. At 3.33tcf, US storage levels are now 4.3% higher than last year and 6.4% higher than the five-year average for the reporting week. Also unsupportive, the Global Forecast System trimmed its two-week HDD forecast from 435 to 443, further below the 462-HDD 30-year average but still exceeding last year's 364 HDDs during the same period. Refinitiv analysts continue to see US demand of 126.3bcf/d outpacing supply of 100.8bcf/d by 25.5bcf/d next week. Cash natural gas prices were mixed today. Henry Hub prices fell one cent to $2.76/mmBtu, and Algonquin citygate prices dropped sharply from $3.50 to $2.93/mmBtu, but Zone 6 prices at the New York citygate rose 2 cents to $2.78/mmBtu.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

NYMEX HO futures continued higher today, adding 0.6% in an upside session and hitting new multi-month highs, consistent with our directional bias. We remain continue to see flat to higher prices, but note that the RSI (69.9) is approaching overbought conditions. There is some headroom yet for the slow stochastics, and all other indicators (outside of the MACD, which is neutral) point higher. We see nearby resistance at today's $1.5501 high, followed by $1.6424, whereas the 9-day ma ($1.4966) and the $1.4000 mark remain nearby support. RBOB futures also continued higher, also consistent with our directional view, adding 0.5% today - but in an inside session as bulls failed to match yesterday's high. We continue to see nearby resistance at $1.5000 and then $1.5427, with $1.3899 and 18-day ma ($1.3840) support. As with HO, the MACD is neutral but all other indicators point north. WTI futures edged up 0.4% today in an upside session, hitting a new multi-month high of $51.28. We look there for nearby resistance, followed by $55.58, and continue to favor upside chances. Nearby support is seen at the 9-day ma ($48.87) and then down at $45.27. The RSI is overbought, but slow stochastics have a small amount of headroom. Lastly, we were favoring the upside for NYMEX NG and futures added 0.5% today, but in an inside session (high low, but also a lower high). Slow stochastics are overcooked but the RSI (53.3) is still very neutral. Still, bullish momentum looks to be flagging. Nearby $1.769 resistance continues to hold, and we'll continue to keep an eye there and then up at $2.898, whereas the 100-day ma ($2.626) and then $2.403 remain nearby support.