PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures continued higher today in a relatively thinly-traded session, despite weakness in US and European shares, indications that OPEC+ compliance fell last month, and a generally bearish monthly oil market report from the EIA, although the US dollar index did fall into negative territory later in the session. As noted in Pipeline, Petro-Logistics estimates that OPEC+ compliance with output cuts fell to about 75% last month, one of the lowest rates since May. Also unsupportive, the EIA released its Short-Term Energy Outlook today, which showed the agency revised down its 2021 global oil demand growth forecast by 220bk/d to 5.56mb/d. Demand is seen growing b 3.31mb/d next year. EIA expects OPEC production to rise from 25.6mb/d last year to 27.2mb/d with the higher production targets and Libyan output growth. The agency expects US oil production to fall by 190kb/d this year to 11.10mb/d, but sees a 390kb/d rise next year to an average of 11.49mb/d. European shares closed lower today amid weaker than expected Italian retail sales data. The FTSE 100 fell 0.7% and the CAC 40 shed 0.2%, while losses in the DAX were more limited at 0.1%. As of this writing, US stock market indexes were mixed with the S&P 500 flat, while the Dow was up 0.1% and the Nasdaq had added 0.2%. The slim gains came despite a miss in the Job Openings and Labor Turnover Survey for November.

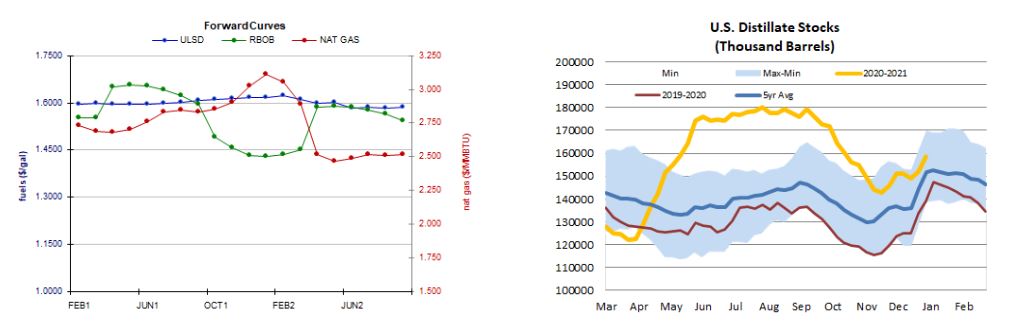

ULSD Forward Curves w/ RBOB & Nat Gas Distillate Stocks

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures on NYMEX strengthened slightly further today with a slight upgrade to the two-week heating degree day forecast (GFS), and some improvement in the 11-15 day outlook (ECMWF), despite a slightly looser market balance expectation for next week (Refinitiv). The GFS sees 456 HDDs over the next two weeks, up from 445 and just shy of the 459-HDD 30-year average - and also well above last year's 395 HDDs during the same period. Also supportive, the latest 11-15 day outlook based on the European model sees some below-normal temperatures in the Pacific Northwest and extending into parts of the Midwest, and mixed near-normal temperatures on the East Coast. Both the 6-10 and, especially, the 1-5 day outlooks remain unsupportive, however, with expectations for above-normal temperatures. Also unsupportive, Refinitiv analysts see total US demand at 125.1bcf/d next week, down from 125.6bcf/d previously, while supply is seen averaging 99.9bcfd (up from 99.8bcf/d previously). Cash natural gas prices were mixed, with Henry Hub prices down by 6 cents to $2.71/mmBtu, but Transco Zone 6 prices in New York up 7 cents to $2.90/mmBtu and Algonquin citygate prices up 30 cents to $4.20/mmBtu. The EIA is due to release its weekly petroleum inventory report tomorrow, and analysts polled by Reuters expect to see a 2.3mb draw from commercial crude oil inventories as the nation's refinery utilization rate rises by 0.2 percentage points to 80.9% of installed capacity. Builds in product inventories are expected, of 2.7mb each for gasoline and distillates.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

Consistent with our directional bias, ULSD futures continued their upward march today, gaining 1.5% - although trade was relatively thin. We hit a fresh high of $1.6011, which becomes nearby resistance - followed by $1.6424 - whereas we continue to see nearby support at the 9-day ma ($1.5294) and then $1.4000. Slow stochastics and the RSI are deep in overbought territory, indicating a consolidation or retracement could be due in the coming sessions. However, we abandoned the RBOB and WTI bulls yesterday and appear to have done so prematurely. Despite a stronger showing by RBOB bears in the previous session, bulls took over and we climbed 2.1% in an upside session today. Accordingly, we'll go back to favoring upside chances until we see stronger evidence that the trend has ended. We see nearby resistance at $1.5613 (today's high), followed by $1.6000, whereas $1.5000 and then the 18-day ma ($1.4207) remain nearby support. Slow stochastics and the RSI are both overbought, whereas the MACD and candlesticks point higher. Again, we acknowledge in WTI that we were premature in abandoning the bulls, with prices rising another 1.8% in an upside session to new multi-month highs. Bulls took out $52.75, and we now look to today's $53.28 high for resistance, still followed by $55.58, whereas $50.54 (reinforced by the 9-da ma) and then $45.27 are seen offering nearby support. Indicators are similar to those in products. We sat on the sidelines regarding natural gas, and a 0.2% uptick today was consistent with this - although we did see intraday strength with a trip up to test $2.898 resistance. We settled in the bottom portion of the daily range, printing a shooting star candlestick that can be a bearish reversal pattern. We'll stick to the sidelines, seeing $2.769 and $2.898 resistance, with 100-day ma ($2.636) and then $2.403 support.