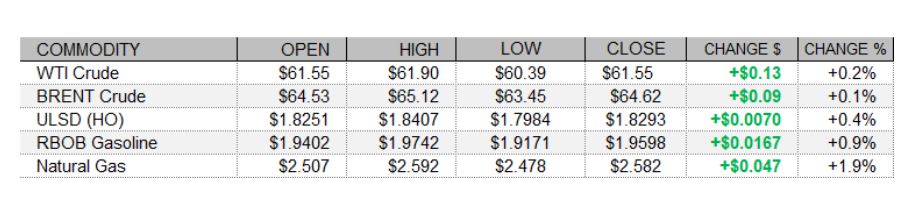

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex saw early weakness following news of tighter coronavirus-related restrictions in parts of England and Germany, but recovered later on, settling higher. Trade in equities and in the US dollar was largely supportive today. Across the pond, while the CAC 40 fell 0.5%, both the DAX and the FTSE 100 gained 0.3%. The pan-European Stoxx 600 added 0.2%. US shares strengthened today despite disappointing existing US home sales figures for February. Sales slowed from a downwardly-revised 6.660mb annualized pace in January to a 6.220m pace in February, below consensus at 6.500m. Nevertheless, shares were rising today. As of this writing, the Dow had gained 0.4%, the S&P 500 had added 0.9%, and Nasdaq futures had climbed 1.5% higher. Also supportive for crude, the US dollar index was down by 0.2%. Equities may have found some support from news that US trial data for the AstraZeneca coronavirus vaccine showed 79% efficacy in preventing symptomatic COVID-19 and there were no indications of increased blood clot risk.

NATURAL GAS | WEATHER | INVENTORIES

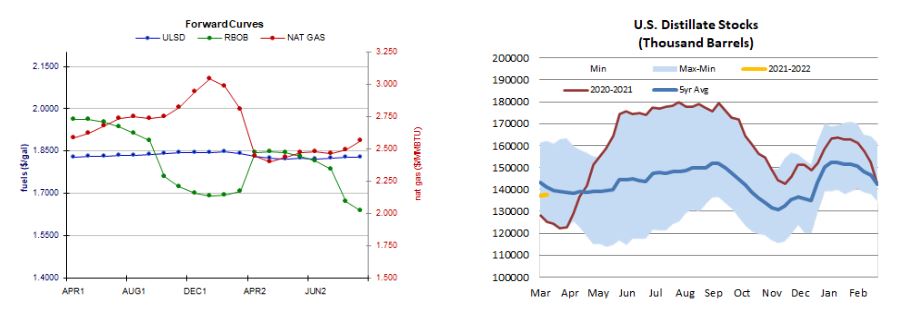

Natural gas futures saw modest strength today despite an unsupportive near-term outlook. The Global Forecast System slashed its HDD forecast for the next two weeks, down from 211 to 184. This is well below last year's 224 HDDs and even further below the 241-HDD 30-year average. The latest 1-5 day ECMWF outlook calls for above-normal temperatures across the eastern half of the country, with especially large deviations above normal in the Northeast and in states just south of the Great Lakes. Refinitiv analysts revised down their total US supply forecast for this week quite sharply, by 2.3 to 98.6bcf/d, while raising their supply forecast by 0.5 to 99.3bcf/d, suggesting 0.7bcf/d injections. The market is seen in a very slight deficit the next week, however, with analysts expecting demand to average 99.4bcf/d while supply averages 99.3bcf/d. The 6-10 day ECMWF outlook calls for above-normal temperatures across the eastern half of the country, but with relatively small deviations over normal temperatures. In the cash market, next-day natural gas prices were mixed. New York citygate prices (Transco Z6) fell by 39 cents to $2.02/mmBtu, but Algonquin citygate prices jumped 93 cents higher to $3.23/mmBtu and benchmark Henry Hub prices gained 8 cents, hitting $2.53/mmBtu.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

Contrary to our downside bias, ULSD futures added 0.4% in an upside session. Most indicators are now neutral, as slow stochastics look to have crossed a bit north of oversold territory. Moving averages remain bullish, whereas a strong ADX indicates a downtrend. We'll stick to a downside bias for the moment, given that we saw a star-shaped candlestick today, and as bulls were unable to take out nearby $1.8330 resistance on a settlement basis. We'll look there and then to the 9-day ma ($1.8965) above, whereas we see support at the 50-day ma ($1.7609) and then at $1.7000 below. RBOB futures added 0.9% today, also in an upside session. Slow stochastics are just north of oversold territory and threatening to cross bullishly. Still, we'll stick to our downside bias for a session longer, seeing support at $1.8973 and then at the 50-day ma ($1.7761), with resistance expected at the 18-day ma ($2.0129) and then up at $2.1700. WTI futures edged up 0.2%, printing a hammer-shaped candlestick with a very thin body, indicating ambivalence. We continue to favor downside chances for the moment, still looking to $59.67 and then $57.21 for support, whereas $63.75 and $66.98 are our nearby resistance levels. Natural gas futures continued higher today in an upside session, taking out the 9-day ma ($2.571) on a settlement basis, closing above said average for the first time since March 4. Stochastics look bullish along with candlesticks. Major averages are neutral, while the MACD is bearish. We are back on the sidelines, seeing next resistance at $2.758 and then at $2.898, whereas the 200-day ma ($2.455) and then $2.403 are nearby support.