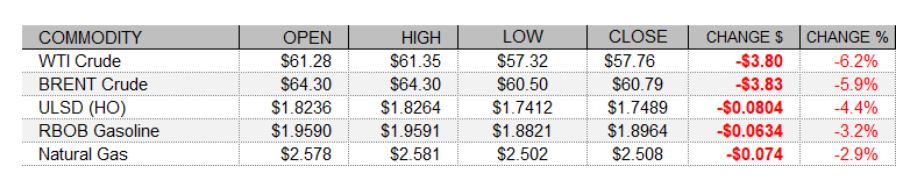

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures tumbled lower today, led by WTI, amid losses in European and US equities, a rally in the US dollar, and news that trial results for the AstraZeneca vaccine may have included outdated information. After doubts were cast over the efficiency of AstraZeneca's vaccine due to outdated information, the pharmaceutical company said that it will publish up-to-date results from its latest vaccine trial within 48 hours. In economic news, US new home sales slowed from an upwardly-revised 948,000 pace in January to 775,000 in February - well below consensus at 875,000. European shares closed flat to lower today with the DAX holding steady, while the CAC 40 and the FTSE 100 both lost 0.4%. As of this writing, US stock market indexes were seeing losses of between 0.2% (S&P 500) and 0.4% (Dow, Nasdaq). Also unsupportive for crude oil prices, the US dollar index was up 0.6%. In supportive news today, Barclays has raised its 2021 oil price forecasts for crude oil by $4/bbl, to $66/bbl for Brent and $62/bbl for WTI.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures turned back south today amid a looser US market balance expectation for next week, a weaker two-week heating degree day forecast, and unsupportive temperature outlooks. The Global Forecast System cut its heating degree day forecast for the next two weeks from 184 to 166, which is well below both the 30-year average of 237 and last year's 224 HDDs over the same period. The latest 1-5 day outlook (EC) calls for well-above-normal temperatures across the eastern half of the country. The 6-10 and 11-15 day forecasts are also unsupportive with above-normal temperatures seen in both the Midwest and the Northeast. Refinitiv analysts now see total US supply of 99.4bcf/d outpacing US demand at 95.8bcf/d next week, implying injections of 3.6bcf/d. In the cash market today, prices at the Henry Hub benchmark rose by two cents to $2.55/mmBtu, while Algonquin citygate prices fell from $2.23 to $2.05/mmBtu, and Transco Zone 6 prices in New York weakened from $2.02 to $1.90/mmBtu. According to a Reuters poll of analysts, estimates for the weekly EIA petroleum inventory report for the week ended March 19 call for a 0.3mb dip in US crude stocks amid a 3.2 percentage point predicted increase in the nation’s refinery utilization rate. Distillate stocks are expected to fall by 0.1mb, while gasoline stockpiles are seen rising by 1.2mb. API petroleum inventories for the same week are due this afternoon at 4:30.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures dropped 4.4% today in a downside session taking out nearby 50-day ma support ($1.7643, becomes nearby resistance) in the process and vindicating our decision to remain bearish. We continue to favor downside chances, and note that neither the RSI nor slow stochastics are yet oversold. Meanwhile, major averages are weakening, and the ADX continues to indicate a strong downtrend. The MACD is neutral. Next support at $1.7000, followed by the 23.6% retracement of the rally from the pandemic lows to the March 9 highs. Meanwhile, we see resistance at the 50-day ma and then up at $1.8330. RBOB futures fell 3.2% today in a downside session, consistent with our directional bias. We continue to favor downside chances. While slow stochastics are entering oversold territory, the RSI still has room to fall. We expect support from the 50-day ma ($1.7831) and from the 23.6% retracement of the rally nearby ($1.7475), whereas the 18-day ma ($2.0129) and then $2.1700 should offer resistance. WTI futures gapped lower and dropped 6.2% lower, consistent with our bearish view. Bears threatened the 38.2% retracement of the rally from the pandemic lows ($57.21) but failed to quite reach it. We'll look there and then to $55.58 for support, seeing as $59.67 was taken out (and this becomes nearby resistance, followed by the 9-day ma ($63.01). Finally, NYMEX natural gas futures shed 2.9% today but in an inside session, not too inconsistent with our neutral view. Trade has been largely sideways over the past seven sessions. Major averages are neutral, as is the RSI, while slow stochastics point higher but the MACD points lower. We see resistance at $2.758 and then $2.898, while the 200-day ma ($2.458) and then $2.403 are seen offering support.