PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures turned back south today with losses of over 3.0% amid a continued rally in the US dollar and mixed trade in European equities, despite supportive economic data releases from the US, gains in US market indexes, and news that the Suez Canal could be blocked for weeks. Reuters reported that a container ship that is blocking the Suez Canal may take weeks to move, according to the salvage company. In US news, the final estimate of fourth quarter GDP showed a 4.3% increase, above the Econoday consensus at 4.1%. Weekly initial jobless claims came in at 684,000, well below the Econoday consensus at 730,000 and down from 781,000 the prior week. As of this writing, US stock market indexes were seeing gains of between 0.1% (Nasdaq) and 0.3% (Dow, S&P 500). European shares closed mixed with the DAX and the CAC 40 both up 0.1%, while the FTSE 100 lost 0.6%. The US dollar index continued higher today and was up 0.4% as of this writing, which is unsupportive for crude prices.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures continued higher today amid a bullish weekly storage report from the Energy Information Administration (EIA), despite a weaker two-week heating degree day forecast and a looser market balance expectation for next week. The EIA reported a 36bcf withdrawal from underground natural gas storage for the week ended March 19, well above forecasts at 25bcf. Total storage levels fell to 1.746tcf, which is 13.1% lower than last year and 4.3% below the five-year average for the reporting week. The Global Forecast System cut its heating degree day forecast for the next two weeks by 6 to 169, which is well below both last year’s 224HDDs over the same period and the 30-year average of 229. The latest 1-5 day outlook (EC) continues to see above-normal temperatures across the eastern half of the country with large deviations above normal temperatures expected on the East Coast. Refinitiv analysts now see total US supply of 98.6bcf/d outpacing US demand at 96.8bcf/d next week, implying larger injections of 1.8bcf/d (compared to yesterday’s forecast at 1.5bcf/d). In the cash market today, prices at the Henry Hub benchmark held steady at $2.56/mmBtu, while Transco Zone 6 prices in New York fell from $2.04 to $1.83/mmBtu and Algonquin citygate prices weakened from $2.12 to $1.93/mmBtu. The 6-10 day weather forecast is more supportive with mixed temperatures seen in the Midwest, while the Northeast is expected to see mostly below-normal temperatures.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

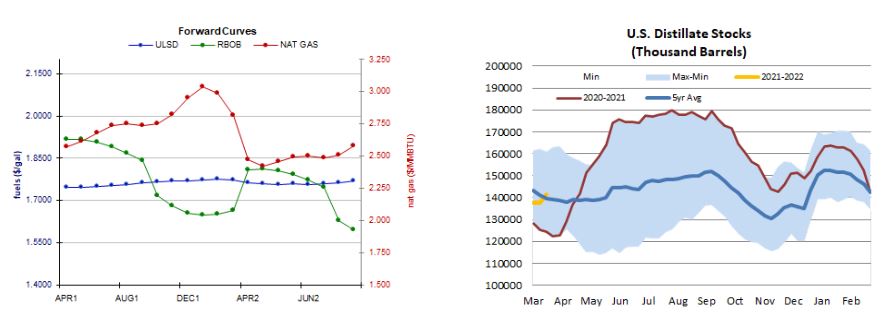

ULSD futures lost 4.3% in a thin-volume downside session (lower low, lower high) – consistent with our bearish bias. Slow stochastics and the RSI are bearish, while the MACD and candlesticks are neutral. Bears took out the 50-day ma ($1.7723) support level, which is our resistance level now, followed by $1.8330, whereas $1.7000 and $1.6553 are our nearby support levels. We remain bearish for now. RBOB futures dropped 3.4% in an inside session (lower high, higher low) – somewhat consistent with our downside bias which we maintain. Slow stochastics continue to point higher, while the RSI is bearish, and the MACD and candlesticks are neutral. Nearby support is seen at the 50-day ma ($1.8000) and then down at $1.7475, with the 18-day ma ($2.0184) and $2.1700 expected to offer resistance. WTI fell 4.3% in an inside session today – consistent with our bearish bias. Bears took out the $59.67 support level and the 50-day ma ($58.95) along the way and we now see nearby support at $57.21 and then at $52.17, while the aforementioned $59.67 and the 9-day ma ($61.70) are seen offering resistance. Technical indicators are similar to those in ULSD, so we are going to continue to favor downside chances for now. Natural gas futures, where we were neutral, added 2.1% in an outside session (higher high, lower low). We are going to stay on the sidelines for now, still seeing nearby resistance at $2.758 and then up at $2.898, whereas the 200-day ma ($2.466) and $2.403 are our nearby support levels. Slow stochastics are neutral, while the RSI points higher, and the MACD is still bearish but looks set to cross bullishly and become neutral.