PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures saw see-saw trade today, opening mostly higher then falling with RBOB leading the way following the weekly EIA report, only to recover late in the session. The weekly EIA inventory report was bullish for crude oil but neutral for propane, unsupportive for distillates, and bearish for gasoline. See our DOE Report for details. European shares settled mixed today, with the DAX losing 0.24% and the CAC 40 edging down 0.01% despite favorable German and French Composite PMI from Markit, while the FTSE 100 gained 0.91% despite a miss in the CIPS/Markit Services PMI for the UK. US stock market index saw mixed trade near the unchanged mark, with the Dow and Nasdaq off less than 0.1% while the S&P 500 was up by less than 0.1% as of this writing. The US dollar index was flat as well. US economic data was disappointing, as the goods and services trade deficit widened from $67.8bn in January to $71.1bn in February, a above expectations at $70.4bn. The Canadian merchandise trade surplus the same month was C$1.04bn, topping expectations at C$1.0bn.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures on NYMEX strengthened today with an upgrade to the heating degree day forecast and a tighter picture of next week's US market balance. The Global Forecast System raised its two-week HDD forecast by 13 to 143, closer to the 30-year average at 176 but still well below last year's 205 HDDs during the same period. Refinitiv analysts raised their total US demand forecast for next week by 0.3 to 90.2bcf/d while trimming their supply forecast by 0.1 to 99.0bcf/d, implying smaller injections of 8.8bcf/d. The next 5 days are still expected to see well above normal temperatures in consuming regions, however, according to the latest 1-5 day ECMWF outlook. Next-day cash natural gas prices strengthened, however, with prices at Henry Hub up one cent to $2.44/mmBtu, Transco Zone 6 prices in New York up 8 cents to $1.85/mmBtu, and Algonquin citygate prices strengthening by 12 cents to $2.02/mmBtu. The EIA is due to report natural gas storage levels for the week ended April 2 tomorrow, and a poll of analysts conducted by Reuters puts expectations at a 21bcf injection. This would be smaller than last year's 30bcf rise, but higher than the 8bcf five-year average.

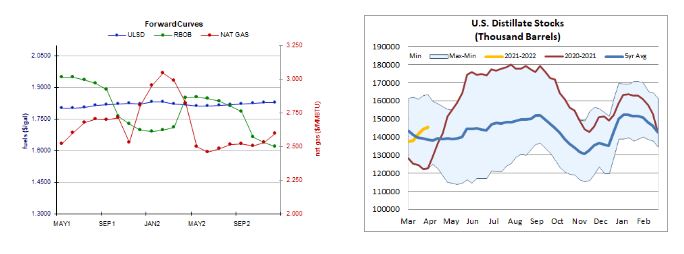

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures opened higher today but fell intraday, only to recover and post gains of 0.8% in a low-volume downside session – consistent with our neutral bias. Slow stochastics point lower and the MACD crossed the zero line and is bearish now, while the RSI and candlesticks are neutral. Bulls took out the 50-day ma ($1.8043), which now becomes nearby support, followed by $1.7295, whereas $1.8330 and $1.9000 are our resistance levels. We remain on the sidelines for now. RBOB futures fell 0.7% in a downside session today – not so consistent with our neutral bias. Slow stochastics are bearish, while the RSI and the MACD are neutral. We remain neutral for now, awaiting further developments. We look to the 50-day ma ($1.8685) and then $1.7475 for support, while the 18-day ma ($1.9922) and $2.1108 are expected to offer resistance. WTI, where we were also neutral, added 0.7% in a downside session – consistent with our view. Slow stochastics point lower, while the RSI, candlesticks, and the MACD are neutral, although the MACD looks set to cross the zero line and become bearish. We continue to see nearby support at $57.21 and then down at $59.67, with the 9-day ma ($60.00 – tested today) and the 18-day ma ($61.24) seen offering resistance. We took a bearish stance yesterday, but NYMEX natural gas futures rose 2.6% in an inside session today with bulls taking out the 200-day ma ($2.501) resistance level, which now becomes nearby support, followed by $2.403. Slow stochastics are bearish, while the MACD is neutral, and the RSI points higher. We are going to continue to favor downside chances for now, awaiting further developments. Resistance is seen at $2.758 and then up at $2.898.