PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude oil and refined products saw modest strength for much of today's session amid geopolitical tensions and weakness in the US dollar index, whereas weakness in equities likely helped limit gains. A Houthi military spokesperson stated that another strike against Saudi Arabian facilities had been carried out, involving 17 drones and 2 ballistic missiles. Targets included Saudi Aramco facilities in Jeddah and Jubail. There was no immediate confirmation from Saudi Arabia and Saudi Aramco made no comment when contacted by Reuters. Also supportive for crude, the US dollar index was down 0.10% as of this writing. On the other hand, European shares lost ground today with the FTSE 100 losing 0.39% and both the DAX and CAC 40 shedding 0.13%. The losses came despite encouraging February Eurozone retail sales data, showing a higher than expected monthly jump of 3.0%. The major US stock market indexes were also losing ground as of this writing, with the Dow down 0.4%, the S&P 500 off 0.2%, and the Nasdaq down 0.5%.

NATURAL GAS | WEATHER | INVENTORIES

NYMEX natural gas futures strengthened some today, with supportive shifts in the temperature outlook. The Global Forecast System sees 152 heating degree days over the next two weeks, up from 139 in the previous forecast and closer to the 30-year average of 156 - but still well below last year's 197 HDDs for the same period. The latest 1-5 day ECMWF outlook calls for well-below-normal temperatures in parts of the Midwest and Northwest, but more mixed temperatures near the Great Lakes and above-normal temperatures along the East Coast. Next-day cash natural gas prices on the East Coast fell, with Algonquin citygate prices falling 7 cents to $1.75/mmBtu and Transco Zone 6 prices in New York falling 13 cents $1.69/mmBtu. Henry Hub prices edged up one cent to $2.48/mmBtu. The 6-10 day ECMWF forecast is supportive, with below-normal temperatures expected across most of the country. Refinitiv analysts see total US demand rising from 91.7bcf/d this week to 92.1bcf/d next week, but supply is expected to rise as well, from 97.6 to 98.0bcf/d, implying no change in the rate of storage injections from 5.9bcf/d.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

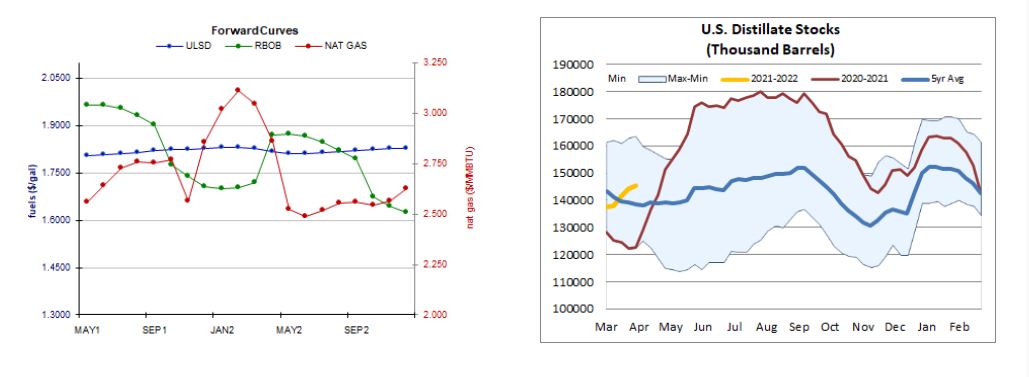

ULSD futures continued sideways, doing nothing to push us off of the sidelines. Futures settled well off of the highs and in the bottom half of the daily range below both $1.8330 and 50-day ma ($1.8167) resistance. We'll continue to keep an eye there, and down at $1.7295 and $1.6553 for support. Although the MACD and ADX still point weakly south, all other indicators are neutral, and we remain neutral. RBOB futures edged up 0.4% in an upside session, settling just a hair above nearby 18-day ma resistance ($1.9664) - now nearby support, followed by the 50-day ma ($1.8915). We look next to the recent $2.0360 high for resistance, followed by $2.1108. Trade remains rangebound, the RSI, slow stochastics, MACD, and candlesticks are all neutral. Major averages are neutral/bullish. We remain neutral. WTI futures added 0.6% today in an outside session (higher high, but also a lower low), and we remain sidelined here as well. Trade remains centered around $59.52 (23.6% Great Recession retracement) in a wedge pattern. A breakout in one direction or another may be due in the coming sessions. We see nearby resistance at the 9-day ma ($59.72), followed by $63.75, whereas $57.21 and then the 100-day ma ($54.33) are expected to offer nearby support. Natural gas futures gapped higher over the weekend and hit a higher high, but came off and settled in the middle of the daily range. Slow stochastics point higher, and candlesticks are trending weakly higher, but the RSI, major averages, and MACD are all neutral. We remain on the sidelines, looking to $2.758 and $2.898 for nearby resistance, whereas the 200-day ma ($2.514) and then $2.403 are nearby support.