PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures hugged the unchanging mark today, spending most of their time south of it and settling in the red. Trade in equities and the US dollar was supportive, whereas the weekly rig counts were unsupportive. In economic news, the final Harmonized Index of Consumer Prices for the Eurozone was left unrevised for March, as expected. The FTSE 100 in the UK rose 0.52%, France's CAC 40 gained 0.85%, and the German DAX rallied 1.34%. In US news, the preliminary University of Michigan consumer sentiment index was a miss, rising from 84.9 to 86.5 but failing to match consensus at 89.0. On the other hand, US housing market data were encouraging today. Housing starts accelerated from an upwardly-revised annualized pace of 1.457m in February to 1.739m, beating the 1.620m consensus. Permits accelerated from an upwardly-revised 1.720m to 1.766m, compared to expectations at 1.750m. As of this writing, the Nasdaq was off 0.01% but the S&P 500 was up 0.19% and the Dow had added 0.31%. The US dollar index was down 0.15%, also supportive for crude. In unsupportive supply-side news, Baker Hughes reported a rise of 7 this week in the US oil rig count, putting it at 344. This is down by 94 from the same week last year.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures on NYMEX saw modest strength today with a tighter expected US market balance next week, despite a downgrade to the two-week heating degree day outlook and an uptick in the rig count. Refinitiv analysts see total US supply averaging 98.1bcf/d next week, unchanged from yesterday's forecast, but now expect demand to average 96.0bcf/d, 1.1bcf/d higher than previously, implying smaller injections into storage of 2.1bcf/d. On the other hand, the Global Forecast System cut its two-week heating degree day forecast from 156 to 146, closer to the 30-year average of 141 and well below last year's 197 HDDs. Taking a regional perspective, the ECMWF continues to see well below normal temperatures for central parts of the country, mostly west of the Mississippi, and more mixed but largely below-normal temperatures on the East Coast. The 6-10 day outlook is slightly more supportive, with below-normal temperatures expected across most of the country, except for parts of coastal New England. In slightly unsupportive news, Baker Hughes reported a rise of 1 in the US natural gas rig count this week, to 94. That's 5 higher than last year at this time.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

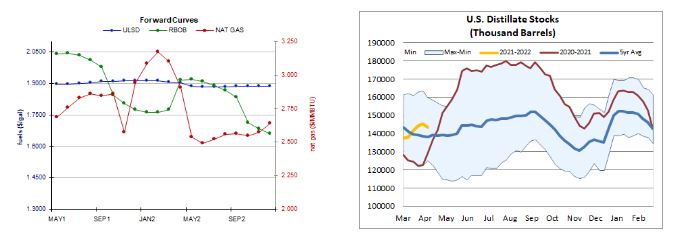

ULSD futures gapped higher, but did hit a higher high before falling back to close down 0.2% in the middle of the daily range. Today's thinly-traded dip in an upside session does little to sway us away from our flat-to-higher price view. The technical picture is mixed, as slow stochastics are overbought, whereas candlesticks and the major averages are neutral, but the MACD and ADX point higher. We continue to expect resistance at $1.9000 and then $1.9695, whereas the 50-day ma ($1.8345) and then $1.8000 are seen offering nearby support. RBOB futures fell 0.6% today, but also in an upside session. As with HO, slow stochastics are overcooked, but the RSI is relatively neutral, as are candlesticks. Major averages and the MACD point higher. We remain neutral/bullish, still looking to $2.1108 and $2.1700 for resistance, with $2.0360 and then 18-day ma ($1.9782) support. WTI fell 0.5% in an upside session, testing the $63.75 resistance level at the highs. We remain neutral/bullish, still seeing resistance at $63.75 and then $67.98, while the 9-day ma ($60.85) and then $57.21 are nearby support. Indicators are similar to those in products, with overbought slow stochastics but bullish major averages and MACD. Lastly, NYMEX natural gas futures continued higher, consistent with our upside bias. Futures added 0.8% in an upside session, settling right at the 100-day ma ($2.680). Slow stochastics have entered overbought territory, but the RSI has plenty of headroom before confirming. Major averages are neutral, as is the MACD, while candlesticks are bullish. We continue to eye $2.758 for nearby resistance, followed by $2.898, whereas the 200-day ma ($2.535) and then $2.403 are expected to offer nearby support.