PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex looked set to extend gains to a third consecutive session and a sixth session in the last seven - but futures came off in the tail end of the session, ending mixed and little changed. Trade in European shares was supportive today, following a stronger than expected Eurozone Composite PMI (Markit). France's CAC 40 climbed 1.4% higher, the FTSE 100 in the UK strengthened 1.68%, and Germany's DAX rallied 2.12%. In US news, ADP reported an increase of 742,000 in private payrolls for last month. While this was 43,000 below the consensus estimate, there was also an upward revision of 48,000 to March payrolls. The ISM Services Index for April was also a miss, seeing a surprise drop from 63.7 to 62.7. This is, however, still quite a strong level. As of this writing, the Dow and S&P 500 were both up 0.3% and the Nasdaq had added 0.2%. The US dollar index was seeing a slight gain of 0.1%. Weekly EIA petroleum inventories were bullish for crude oil and supportive for distillates, but neutral for propane and unsupportive for gasoline. See our DOE Report for details.

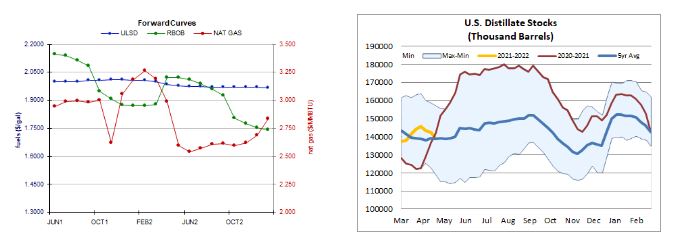

ULSD Forward Curves w/ RBOB & Nat Gas US Distillate Stocks

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures weakened slightly today despite a steady degree day forecast and tighter expected US market balance next week. The Global Forecast System sees 153 degree days over the next two weeks (86 heating and 67 cooling), up by 1 from the previous forecast and above the 30-year average of 141 - but below last year's 172 degree days during the same period. The National Hurricane Center expects no tropical cyclone activity in the Atlantic over the next 48 hours. Next-day cash natural gas prices were mixed, as Algonquin citygate prices fell 40 cents to $2.45/mmBtu, but Transco Zone 6 prices rose 7 cents to $2.45/mmBtu and benchmark Henry Hub prices added 4 cents, hitting $3.00/mmBtu. Refinitiv analysts raised their total US demand forecast for next week by 0.7 to 87.2bcf/d while trimming their supply forecast by 0.1 to 97.4bcf/d, implying smaller injections of 10.2bcf/d. The EIA is due to release its US natural gas storage report for the week ended April 30 tomorrow. Analysts surveyed by Reuters expect to see an 81bcf injection that would match the five-year average but fall short of last year's 103bcf rise.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

ULSD futures gapped higher but fell intraday to still settle 0.2% higher in an upside session – consistent with our bullish bias. We saw a new multi-year high of $2.0278 in today’s session, which now becomes our nearby resistance level, followed by $2.0462, whereas $1.9695 and the 9-day ma ($1.9369) are expected to offer support. Slow stochastics and the RSI are quite neutral while the MACD and candlesticks are bullish. We continue to favor the upside for now. RBOB futures, where we were also bullish, gapped higher and fell intraday to close unchanged in an upside session. Slow stochastics have crossed bullishly in overbought territory, while the RSI is neutral and does not confirm overbought conditions (66.8). We are going to remain bullish for now, still seeing nearby resistance at $2.1700 and then up at $2.2000, while $2.1108 and the 18-day ma ($2.0408) are seen offering support. Similar to products, WTI gapped higher but fell off the highs to settle 0.1% lower in an upside session. Slow stochastics crossed bullishly in neutral territory, and the MACD also points higher, while the RSI is neutral. We are going to remain bullish for a bit longer, still seeing nearby support at $63.75 and then down at the 18-day ma ($62.97), while $66.85 and $67.98 are our nearby resistance levels. Finally, NYMEX natural gas futures fell 1.0% in a downside session today – not so consistent with our neutral/bullish bias. Slow stochastics and the RSI both point lower, while the MACD is bullish and candlesticks are neutral. We fall back onto the sidelines, looking to $2.898 and then $2.758 for support, while $3.171 and $3.316 are seen offering resistance.