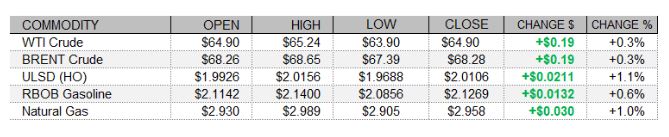

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude futures opened weaker but recovered later in the session amid strength in US and European shares and weakness in the US dollar, despite mostly misses in US and European economic data releases and an unsupportive weekly US rig count update from Baker Hughes. While German industrial production and Italian retail sales were a beat, the German merchandise trade balance, French industrial production, and French merchandise trade deficit were all misses or worse than previously. Nevertheless, European shares closed higher with the CAC 40 up 0.45%, the FTSE 100 up 0.76%, and the DAX rallying 1.34%. Also a miss was today labor market data for our neighbors to the north. The Canadian unemployment rate saw a surprisingly large jump from 7.5% to 8.1% last month. The US labor market report for April was also disappointing. Nonfarm payrolls rose by 226,000 - far short of the 998,000 expectation, and the unemployment rate saw a surprise rise to 6.1% rather than falling from 6.0% to 5.8%, as expected. Nevertheless, US shares were rising as of this writing. The Dow was up 0.49%, the S&P 500 had gained 0.64%, and the Nasdaq was trading 0.82% higher. Also supportive was a 0.73% tumble in the US dollar index, hitting its lowest levels since late February. Meanwhile, Baker Hughes reported a rise of 2 in the US oil rig count this week, to 344, which is now 52 higher than last year's low levels.

NATURAL GAS | WEATHER | INVENTORIES

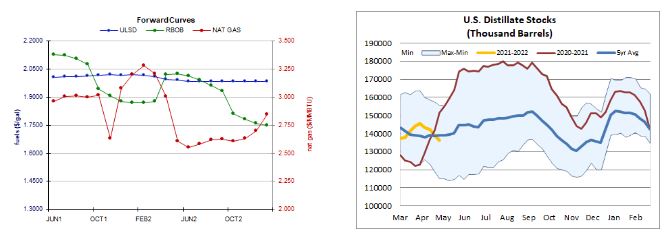

NYMEX natural gas futures saw modest strength today with a slightly tighter US market balance expectation for next week and a slightly stronger two-week degree day forecast, despite a jump in the rig count. Baker Hughes reported a jump of 7 in the US natural gas rig count this week, putting it at 103 - which is 23 higher than last year at this time. Refinitiv analysts see total US demand averaging 88.1bcf/d next week, up by 0.4bcf/d from the previous estimate, and Refinitiv cut its total US supply forecast by 0.1 to 97.2bcf/d, implying smaller injections of 9.1bcf/d. The Global Forecast System raised its two-week total degree day forecast from 153 to 156 (86 heating and 70 cooling), which is above the 30-year average of 140, but below last year's 172 degree days. Cash natural gas prices fell today, with benchmark Henry Hub prices down 9 cents to $2.90/mmBtu, Zone 6 prices in New York shedding 4 cents to hit $2.39/mmBtu, and Algonquin citygate prices dropping 40 cents to $2.40/mmBtu. The National Hurricane Center expects no tropical cyclone activity in the Atlantic over the next 48 hours.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

NYMEX HO futures rose 1.1% today but in an outside session, as we saw both a lower low and a higher high. Slow stochastics, the RSI, the ADX, and candlesticks are all neutral, while the major averages and MACD point higher. We'll stick to the sidelines, still looking to $2.0278 (recent high) and then $2.0462 for resistance, while $1.9695, followed closely by the 9-day ma ($1.9642) remain nearby support. RBOB futures added 0.6% but in a downside session (lower high and a lower low), doing nothing to push us away from our neutral stance. Slow stochastics look bearish, while the RSI is neutral, and candlesticks are neutral as well, but the MACD points higher. We continue to look to $2.1108 and then to the 18-day ma ($2.0570) for support, while $2.1700 and then $2.2000 are our nearby resistance levels. WTI saw an even slimmer gain of 0.3% today in a downside session. Bears threatened but couldn't quite reach $63.75 support, and we settled well off of the lows and in the bottom half of the range - as well as above the 9-day ma ($64.52). We see nearby support at both of these, whereas $66.85 and then $67.98 are expected to offer resistance. We remain neutral. We are also sidelined regarding NYMEX natural gas, and futures continue to go nowhere. Prices rose 1.0% in an outside session (lower low, but a higher high) today, and technical indicators are mixed. We see nearby resistance at $3.171 and then at $3.316, with $2.898 and $2.758 support.