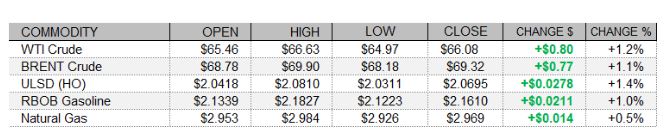

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude futures posted a fourth consecutive session of gains, following a bullish monthly oil market report from the International Energy Agency and with strength in European shares - led by the FTSE 100 following encouraging UK GDP data. Today's gains came despite strength in the US dollar index and a sell-off in equities following stronger than expected consumer price inflation figures, and despite bearish crude stock data in the weekly EIA report. Figures were fairly neutral for distillates and gasoline. The FTSE 100 closed 0.82% higher, outpacing a 0.20% gain in the DAX and a 0.19% rise in the CAC 40. In US news, the Consumer Price Index (CPI) jumped 4.2% higher year-on-year last month, above expectations at 3.6%. Core prices strengthened 3.0% year-on-year, also above the 2.3% forecast. The FOMC has said it would allow inflation to run above 2% for some time, in order to firmly anchor inflation expectations (and support the recovery). As of this writing, the Dow had lost 1.33%, the S&P 500 had fallen 1.60% and the Nasdaq had sold off 2.14%. Also unsupportive for crude, the US dollar index had rallied 0.65%. The major Colonial Pipeline lines remain shut following a ransomware cyberattack last weekend. The DOT says it has assessed ship availability to carry product from the Gulf Coast to the East Coast, and that it is ready to review any Jones Act waiver requests.

NATURAL GAS | WEATHER | INVENTORIES

NYMEX natural gas futures hugged the unchanged mark in today's session, mostly seeing modest strength despite a weaker degree day forecast and loosening picture of next week's US market balance. The Global Forecast System sees 134 degree days (51 heating and 83 cooling) over the next two weeks, down from 138 previously. This is now below the 138-DD 30-year average and also last year's 151 degree days. Also unsupportive, Refinitiv analysts cut their total US demand forecast for next week by 5.6bcf/d, from 87.0 to 81.4bcf/d, while raising their supply forecast by 0.2 to 97.5bcf/d. This implies injections of 16.1bcf/d, compared to 10.3bcf/d previously. In the cash market, next-day natural gas prices were mixed, as Transco Zone 6 prices in New York added one cent, reaching $2.46/mmBtu, while Henry Hub prices shed 2 cents to reach $2.91/mmBtu, and Algonquin citygate prices dropped 28 cents lower to $2.37/mmBtu. The National Hurricane Center expects no tropical cyclone activity in the Atlantic over the next 48 hours.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

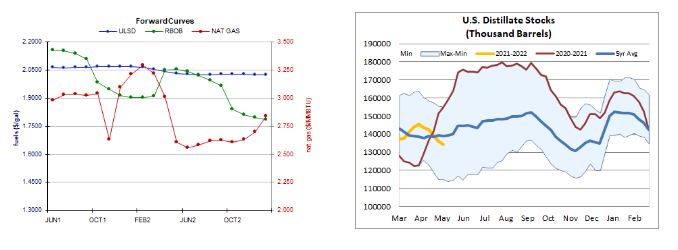

ULSD futures added 1.4% in an upside session today, not so consistent with our neutral bias. Slow stochastics have crossed bullishly in neutral territory, while the RSI is still overbought. Candlesticks, the MACD, and moving averages all point higher. We are going to stay on the sidelines for a bit longer, awaiting further bullish confirmation. Bulls did take out the $2.0462 resistance level, which now becomes nearby support, followed by the 9-day ma ($2.0007), whereas $2.0810 (fresh multi-year high) and $2.1000 are our nearby resistance levels. RBOB futures rose 1.0% higher in an upside session today. Slow stochastics and candlesticks are neutral, while the RSI and the MACD point higher. We are going to keep our neutral stance for a bit longer, still seeing nearby support at $2.1108, followed by the 18-day ma ($2.0743), while $2.1904 and $2.2170 are expected to offer resistance. WTI, where we were also neutral, gapped higher and rose 1.2% in an upside session. Slow stochastics are neutral, while the RSI, candlesticks and the MACD are bullish. We remain neutral for now, still looking to $66.85 and then $67.98 for resistance, with the 9-day ma ($65.02) and $63.75 seen offering support. Lastly, NYMEX natural gas futures edged up 0.5% in a slight upside session today, somewhat consistent with our neutral bias which we maintain. Candlesticks have been moving sideways for the past ten sessions. Nearby support is seen at $2.898 and then down at $2.758, whereas $3.171 and $3.316 remain our nearby resistance levels.