PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex strengthened for a second session today, accelerating gains amid weakness in the US dollar index, strength in US and European shares, and a bullish oil price forecast from Goldman Sachs, despite the extension of an Iranian nuclear program monitoring agreement. Iran and the IAEA extended a recently-expired monitoring agreement for one month. Indirect US-Iranian negotiations resume in Vienna this week. On the other hand, the FTSE 100 gained 0.48% and the CAC 40 climbed 0.35% higher today. The Frankfurt exchange was closed for a holiday. US shares were seeing stronger gains as of this writing, with the Dow up 0.57%, the S&P 500 having gained 1.03%, and the Nasdaq trading 1.39% stronger. Also supportive for crude, the US dollar index was down 0.12%. Also supportive, and as noted in Pipeline this morning, Goldman Sachs inelastic supply and stronger vaccine-driven demand maintaining a case of higher oil prices, seeing $80/bbl Brent prices by the fourth quarter, even with an "aggressive" assumption for Iranian oil exports.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures edged lower today with a lower nuclear power outage rate and a looser US market balance expectation on the one hand, but a stronger two-week cooling degree forecast on the other. The nuclear power outage rate fell from 10% to 5% today, which is well below last year's 11% outage rate and the 9% five-year average. Also unsupportive, Refinitiv analysts raised their total US demand forecast for this week by 0.2bcf/d to 85.0bcf/d, but raised their supply forecast by a larger 0.7bcf/d to 97.6bcf/d, implying larger 12.6bcf/d injections. The market is seen loosening further next week, as supply holds steady while demand drops 0.4bcf/d to 84.6bcf/d. Next-day cash natural gas prices were mixed, with Henry Hub prices shedding 2 cents to hit $2.84/mmBtu, while Algonquin citygate prices held steady at $2.40/mmBtu and Transco Zone 6 prices in New York rose 4 cents to $2.47/mmBtu. In a supportive development today, the Global Forecast System raised its two-week cooling degree day forecast by 8 to 144, which is well above the 89 CDDs seen last year, and also the 103-CDD 30-year average. The National Hurricane Center expects no tropical cyclone formation over the next 48 hours. Tropical Storm Ana developed on Saturday, but weakened to a tropical depression on Sunday.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

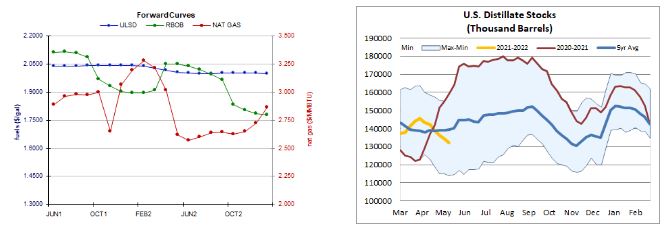

Contrary to our downside bias, ULSD futures continued higher today. Bulls took out both 18-day ma ($2.0066) and the 9-day ma ($2.0250) - which was nearby resistance, taking us 2.7% higher. Slow stochastics look set to re-cross, but well outside of oversold territory, while the RSI is bullish with plenty of room overhead. We abandon the bears, taking a neutral stance for now, seeing next resistance at $2.0462 and then $2.0810, whereas the 9-day ma ($2.0249) and then $1.9695 are seen offering nearby support. RBOB futures also strengthened for a second, upside session, and bulls managed to take out $2.1108 resistance along with the 9-day ma ($2.1148) but not quite the 18-day ma ($2.1178). We see next resistance at the recent $2.2170 high, followed by $2.2500, whereas $2.1108 and then the 50-day ma ($2.0383) are our nearby support levels. As with HO, we'll adopt a neutral stance. We'll do the same with WTI, where bulls made an even stronger showing. We gapped up and over $63.75 resistance over the weekend, and went on to take out both the 18-day ma ($64.79) and the 9-day ma ($64.66). We look to $66.85 and then $67.98 (recent high) for resistance, whereas $63.75 and then the 50-day ma ($62.62) become nearby support. We favored downside chances for natural gas and here, at least, we did see a 0.7% dip with a sharp gap lower over the weekend. Slow stochastics are now oversold, while the RSI (50.2) is quite neutral. Major averages are bullish, while candlesticks are bearish. We remain bearish for now, seeing $2.758 and then 50-day ($2.738) support, with $2.898 and then $3.171 resistance.