PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures settled in the black today amid gains in global shares and weakness in the US dollar index. Today's headline was the US Employment Situation report for May, which was mixed. A 559,000 rise was reported in the nonfarm payrolls, below the 650,000 consensus, while April payrolls were revised up by 12,000. The unemployment rate (U-3) fell from 6.1% to 5.8%, below the 5.9% expectation. The labor force participation rate fell from 61.7% to 61.6%. The Canadian Labor Force Survey showed a 68,000 drop in employment for the month of May, while forecasts called for a smaller decline of 20,000. The unemployment rate in Canada rose from 8.1% to 8.2%, as expected. The Canadian Ivey PMI came in at 64.7 in May, below the Econoday consensus at 65.0. Also unsupportive, US factory orders fell 0.6% in April, while forecasts called for a 0.1% increase. As of this writing, US stock market indexes were seeing gains of between 0.4% (Dow) and 1.5% (Nasdaq). European shares closed higher today with the FTSE 100 and the CAC 40 up 0.1%, while the DAX added 0.4%. Also supportive for crude oil prices, the US dollar index was down 0.4% this afternoon. In supply-side news today, Baker Hughes reported no change in the US oil rig count this week, keeping it at 359.

NATURAL GAS | WEATHER | INVENTORIES

NYMEX natural gas futures rebounded today amid a drop in the US rig count, despite a looser expected US market balance for next week. Baker Hughes reported a drop of 1 in the US natural gas rig count, putting it at 97. For just next week, Refinitiv analysts cut their total US supply forecast by 0.4bcf/d to 97.8bcf/d, while cutting their demand forecast by 1.0bcf/d to 88.0bcf/d, implying larger 9.8bcf/d injections. The nuclear power outage rate was steady today at 3%, which is lower than last year's 7% outage rate and the 6% five-year average. The Global Forecast System kept its CDD forecast for the next two weeks at 170, which is well above last year's 146 CDDs and the 30-year average of 140. In the cash market, next-day natural gas prices softened. Henry Hub prices fell 8 cents to $3.01/mmBtu, Transco Zone 6 prices in New York fell 5 cents to $2.15/mmBtu, and Algonquin citygate prices dropped 34 cents to $1.91/mmBtu.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

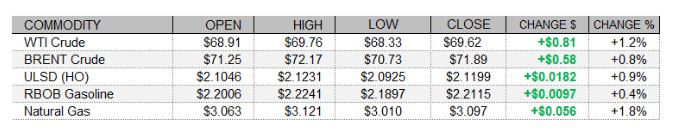

ULSD futures rose 0.9% in an inside session today (lower high, higher low) – somewhat consistent with our bullish bias which we maintain. Slow stochastics are bullish but look set to become overbought, and the RSI, the MACD, and candlesticks all point higher. We continue to see nearby resistance at $2.1236 (yesterday’s high) and then up at $2.1415, while $2.0810 and $2.0462 are seen offering support. RBOB futures, where we were also bullish, added 0.4% in an upside session (higher high, higher low). Slow stochastics are overbought now, while the RSI, the MACD and candlesticks are all bullish. We remain bullish, still looking to $2.2170 and then $2.2500 for resistance, while $2.1108 and the 50-day ma ($2.0653) are expected to offer support. WTI futures jumped 1.2% higher in an upside session today – consistent with our upside bias. We saw a fresh multi-year high at $69.76. We remain bullish, still seeing nearby resistance at $73.29 and then up at $75.00, while $67.98 and $66.85 are our nearby support levels. Lastly, we took a neutral stance yesterday and natural gas futures rose 1.8% today but did so in an outside session (higher high, lower low), which is consistent with our bias. Slow stochastics are bearish, while the RSI and the MACD point higher, and candlesticks are neutral. We continue to see nearby resistance at $3.171 and then up at $3.316, with $2.898 and $2.758 seen offering support.