PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crude oil and refined products futures hugged the unchanged mark today, mostly spending time just south of it and ending in the red, with losses of under one percent. Trade in European shares was mixed, as the DAX fell 0.10% following a miss in headline German manufacturers orders, while the CAC 40 gained 0.43% and the FTSE 100 rose 0.12% amid stronger than expected UK home price appreciation. As of this writing, the major US stock market indexes were mixed as well, with the Nasdaq up 0.2%, while the S&P 500 was down 0.3% and the Dow had lost 0.4%. The US dollar had depreciated by 0.20% against a basket of currencies, which is supportive for crude prices. Also supportive today were comments from the OPEC Secretary General. Mohammad Barkindo said that OPEC expects to see further OECD oil stock draws in the months ahead amid vaccine rollouts and massive fiscal stimulus, although uneven global vaccine availability, coronavirus outbreaks, and high inflation pose risks to demand.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures lost some ground today despite a stronger two-week cooling degree day forecast and a higher nuclear power outage rate. The Global Forecast System sees 180 CDDs over the next two weeks, up from 170 in the previous outlook and elevated compared to the 30-year average of 147. Also supportive, the nuclear power outage rate rose to 5% from 3% yesterday, although this is low compared to the 7% five-year average and last year's 9% outage rate. Refinitiv analysts expect total US supply of 98.3bcf/d to outpace total US demand of 88.2bcf/d this week, implying 10.1bcf/d injections. Benchmark Henry Hub cash price held steady at $3.01/mmBtu, while Transco Zone 6 prices in New York shot up 57 cents to $2.72/mmBtu and Algonquin citygate prices jumped 99 cents higher to $2.90/mmBtu. Next week, Refinitiv analysts see demand strengthening by 0.7bcf/d to 88.9bcf/d, while supply falls by 0.1bcf/d to 98.2bcf/d, implying smaller injections of 9.3bcf/d into storage. Out in the Atlantic, the National Hurricane Center expects no tropical cyclone formation over the next 48 hours.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

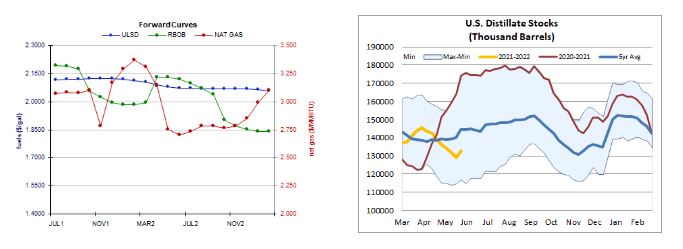

ULSD futures, where we favored upside chances, shed 0.2% today - but we did see a higher high and a higher low, making it an upside session. Today's high was also a fresh multi-year high of $2.1315, which becomes nearby resistance followed closely by $2.1415. We expect nearby support at the 9-day ma ($2.0776), followed by $2.0462. We remain bullish for now, but note that slow stochastics have entered overbought territory. There is no confirmation from the RSI. RBOB futures were less kind to our directional bias, falling 0.5% in a downside session (lower high and a lower low), causing overbought slow stochastics to cross for a sell signal - albeit without confirmation of overbought conditions from the RSI. Still, a rounded top appears to be forming. We'll await stronger evidence that the trend has ended, however, and will continue to look to $2.2170 and then $2.2500 for resistance, with $2.1108 and then 50-day ma ($2.0709) support. As with HO, WTI hit a fresh multi-year high of $70.00 in an upside session today, although we settled off of those highs and down 0.6%. Also similar to HO, slow stochastics are overbought and threatening to cross for a sell signal but without confirmation from the RSI. We'll remain neutral/bullish, seeing resistance at today's $70.00 high, followed by $73.29, while the 9-day ma ($67.74) and then $63.75 should offer support. NYMEX natural gas futures, where we are neutral, continued to move sideways today. Futures lost 0.9% in an inside session (higher low, but also a lower high). Indicators are mixed with bearish slow stochastics but a neutral/bullish MACD and bullish major averages. We see nearby resistance at $3.171 and then $3.316, whereas $2.898 and $2.758 are our nearby support levels.