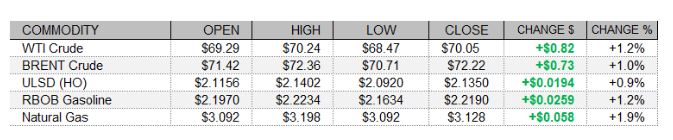

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Petroleum futures rebounded today despite a bearish revision to the 2021 global oil demand forecast in the EIA's Short-Term Energy Outlook, mixed trade in global equities, and strength in the US dollar index. The EIA released its June STEO today, in which the agency cut its 2021 global oil demand growth forecast by 10kb/d to 5.41mb/d and cut its 2022 growth estimate by 90kb/d to 3.64mb/d. The EIA expects US crude oil production to fall by 230kb/d to 11.08mb/d this year, which is a lower drop compared to the previous estimate of 290kb/d. Production is expected to average 11.8mb/d in 2022. Reuters reported that the US Secretary of State Antony Blinken has said that hundreds of US sanctions on Tehran would remain in place even if a nuclear deal between the US and Iran is reached. In North American economic news, the Canadian merchandise trade surplus for the same month was C$0.59bn, while expectations called for a deficit of C$0.8bn. The US international trade in goods and services deficit came in at $68.9bn for April, slightly narrower than the $69.0bn consensus. Also supportive, the US Job Openings and Labor Turnover Survey (JOLTS) put openings at 9.286m in April, beating expectations at 8.045m and up from an upwardly-revised 8.288m in March. As of this writing, the Dow was down 0.02%, while the S&P 500 had edged up 0.02% and the Nasdaq had added 0.20%. European shares closed mixed today with the DAX down 0.23%, whereas the CAC 40 added 0.11% and the FTSE 100 rose 0.25%. The US dollar index was up 0.2% as of this writing, which is unsupportive for crude oil prices.

NATURAL GAS | WEATHER | INVENTORIES

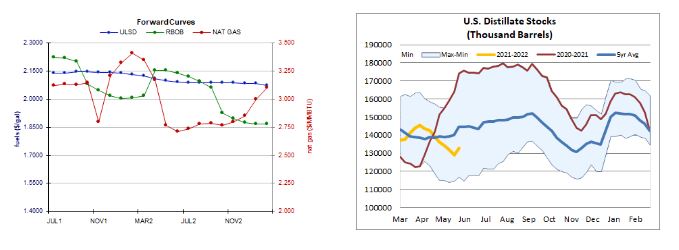

Natural gas futures turned back north today amid a higher nuclear power outage rate, a tighter US market balance expectation for next week and a stronger two-week cooling degree day forecast. The Global Forecast System raised its cooling degree day forecast by 7 to 187 for the next two weeks, which is well above both the 30-year average of 149 CDDs and last year’s 149 cooling degree days over the same period. Refinitiv analysts now see total US supply of 98.6bcf/d outpacing US demand at 89.7bcf/d next week, implying smaller injections of 8.9bcf/d (compared to yesterday’s forecast at 9.3bcf/d). The nuclear power outage rate rose from 5% to 6% today, which is still below both last year's 8% outage rate and the 7% five-year average rate. Next-day natural gas prices were mixed as prices at the Henry Hub benchmark fell by 3 cents to $2.98/mmBtu, while Transco Zone 6 prices in New York rose 15 cents to $2.87/mmBtu and Algonquin citygate prices jumped 60 cents higher to $3.50/mmBtu. The National Hurricane Center does not expect any Atlantic tropical cyclone activity over the next 48 hours. According to a Reuters poll of analysts, estimates for the weekly EIA petroleum inventory report for the week ended June 4 call for a 2.0mb draw from US crude stocks amid a 0.6 percentage point predicted increase in the nation’s refinery utilization rate. Distillate stocks are expected to increase by 1.4mb and gasoline stockpiles are expected to see a build of 0.7mb. API petroleum inventories for the same week are due this afternoon at 4:30.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

We stuck to our upside bias yesterday, and while things did not look good early on, ULSD prices recovered and we hit a new multi-year high of $2.1381, settling 0.9% higher in today's outside session. Nearby support at the 9-day ma ($2.0888) held at the lows. We continue to favor flat-to-higher price action, with the RSI yet unable to confirm overbought conditions given by slow stochastics. We see nearby resistance at $2.1415, followed by $2.2000, whereas $2.0462 follows the 9-day ma as support. RBOB futures rose 1.2% today, also in an outside session. Indicators are similar, with overbought slow stochastics but no confirmation from the RSI, and with bullish moving averages and MACD. We remain neutral/bullish, seeing $2.2241 and then $2.5000 resistance, while $2.1108 and the 50-day ma (2.0759) remain nearby support. Unlike with HO, where bulls were unable to surpass the high set two sessions ago, WTI bulls did succeed, hitting a fresh high of $70.19, which becomes nearby resistance followed by $73.29. The 9-day ma ($68.19) and $63.75 remain nearby support. We remain neutral/bullish. NYMEX natural gas futures gapped higher overnight and went on to trade at their strongest levels since February 18, and above nearby $3.171 resistance - but came off and settled within the recent trading range. We remain neutral for now, seeing $3.171 and then $3.316 resistance, with $2.898 and $2.758 remaining nearby support.