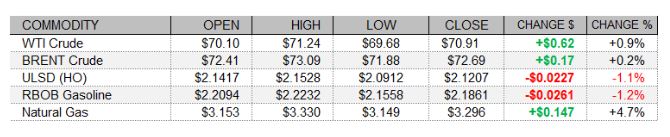

PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

Crack spreads narrowed today as crude futures posted modest gains while refined products futures lost ground. The gains in crude came despite a jump of over 0.5% in the US dollar index as of this writing, and mixed trade in the major US stock market indexes, as well as a rise in the US oil rig count. US data were encouraging today, as the University of Michigan preliminary June consumer sentiment index came in at 86.4, beating forecasts at 84.0 and improving from 82.9 last month. Nevertheless, as of this writing the Dow was down 0.26% and the S&P 500 had lost 0.09%, while the Nasdaq had edged up 0.03%. Trade in European shares today was supportive, with the FTSE 100 gaining 0.65%, the DAX rising 0.78%, and the CAC 40 climbing 0.83% higher. In unsupportive supply-side news today, Baker Hughes reported a rise of 6 in the US oil rig count this week, to 365 - which is 166 higher than last year. In other news, Reuters reports that the EPA is considering ways to provide relief to US oil refiners from biofuel blending mandates, and that ethanol (D6) RINs prices fell 15% from the previous session, to $1.70, later steadying at $1.85.

NATURAL GAS | WEATHER | INVENTORIES

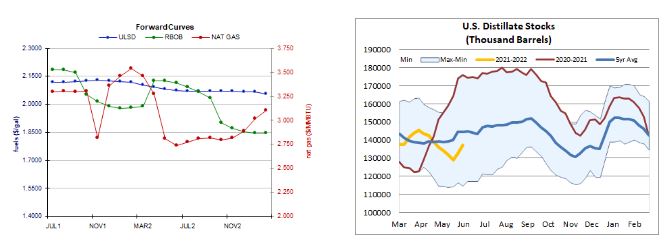

Natural gas futures strengthened today with a stronger cooling degree day forecast, increased nuclear power outages, a dip in the rig count, and a slightly tighter forecast for next week's US market balance. Things remain quiet in the Atlantic, with the National Hurricane Center expecting no tropical cyclone formation over the next 48 hours. The nuclear power outage rate rose by two percentage points to 7% today, matching last year's outage rate and topping the 6% five-year average. Cash natural gas prices saw flat-to-lower trade, with Henry Hub holding at $3.13/mmBtu, while Zone 6 prices in New York fell 10 cents to $2.20/mmBtu and Algonquin citygate prices shed 4 cents, reaching $2.38/mmBtu. In supportive news today, the Global Forecast System raised its two-week Cooling Degree Day forecast by 7 to 195, which is well above last year's 149 CDDs and also the 156-CDD 30-year average. Also supportive, Refinitiv analysts kept their total US supply forecast for next week steady at 98.6bcf/d, while nudging up their demand forecast by 0.1bcf/d to 90.1bcf/d, implying slightly smaller injections of 8.5bcf/d. In supportive supply-side news, Baker Hughes reported a dip of 1 in the US rig count this week, to 96.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

NYMEX ULSD (HO) futures fell 1.1% in a downside session today. Slow stochastics are bearish, falling from overbought territory, but the RSI remains more neutral. Meanwhile, major averages, the MACD, and the ADX continue to point higher. We'll maintain our neutral/bullish stance for now, seeing resistance at the recent $2.1560 high, followed by $2.2000, while the 9-day ma ($2.1160) and then $2.0462 remain nearby support. Similarly, RBOB futures lost 1.2% today in a downside session. Slow stochastics look bearish, and a rounded top appears to have developed. The MACD is set to cross and go from bullish to neutral, but moving averages continue to point higher. We fall back to the sidelines, looking out for bearish confirmation. We see nearby support at $2.1108, followed by the 50-day ma ($2.0891), while $2.2365 (recent high) and then $2.5000 remain our nearby resistance levels. WTI futures were kinder to our directional bias, strengthening 0.9% in an upside session and hitting a fresh multi-year high of $71.24. This becomes nearby resistance, followed by $73.29, while we expect support from the 9-day ma ($69.49), followed by $63.75. Finally, NYMEX natural gas futures strengthened 4.7% in an upside session. We side with the bulls, but note that a retracement could be possible in the following session. We see next resistance at $3.171 and then $3.316, whereas $2.898 and then $2.758 remain our nearby support levels.