PETROLEUM COMPLEX (WTI | BRENT | ULSD | RBOB)

The complex strengthened today, with the gasoline crack widening in a manner consistent with weekly EIA inventory figures. The agency reported a surprisingly large draw from crude stocks for the week ended June 18 and a surprise draw from gasoline inventories, as well as a smaller-than-normal build in combined propane and propylene stocks, but an as-expected build in distillates. See our DOE Report for more. Trade in European shares today was unsupportive, as indexes fell despite generally encouraging economic data release. The flash June Eurozone Composite PMI strengthened from 56.9 to 59.2, beating expectations at 58.8, and the index for Germany rose from 56.2 and past consensus at 57.5 to 60.4. Nevertheless, the DAX fell 1.15%. Despite a miss in the flash France Composite PMI (57.1 vs 59.0 expected), losses in the CAC 40 were smaller at 0.91%. The FTSE 100 in the UK slipped 0.22% lower. US shares were mixed as of this writing, with the Dow off 0.04%, but with the S&P 500 up 0.09% and the Nasdaq having gained 0.23%. The US dollar index was steady.

NATURAL GAS | WEATHER | INVENTORIES

Natural gas futures strengthened further today with a stronger degree day forecast and a tightening picture of next week's market balance, as well as a rise in the nuclear power outage rate. The nuclear power outage rate doubled to 4% today, although this is below the 5% five-year average rate and also last year's 7%. Cash natural gas prices were mixed, with Henry Hub up 6 cents to $3.21/mmBtu and Transco Zone 6 (New York) up one cent to $2.59/mmBtu, but with Algonquin citygate prices falling 17 cents to $2.48/mmBtu. In supportive news, the Global Forecast System raised its two-week CDD forecast by 9 to 217, which is well above both last year's 198 CDDs and also the 30-year average of 182. The NHC is tracking a disturbance a few hundred miles east of the Windward Islands, but gives it a low chance of 10% for tropical cyclone formation over the next 48 hours. The EIA is due to release natural gas storage figures for the week ended June 18 tomorrow morning, and a poll of analysts conducted by Reuters calls for a 66bcf injection. This would be smaller than the 83bcf five-year average and well below last year's 115bcf rise in storage levels.

ENERGY TECHNICALS (WTI | ULSD | RBOB | NG)

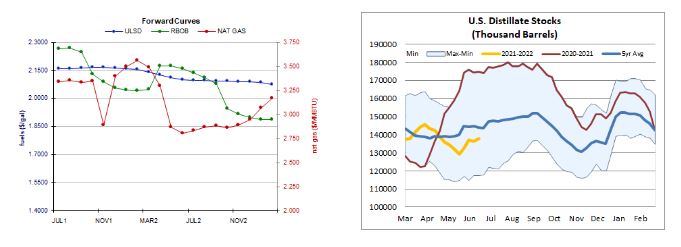

ULSD futures saw a fresh multi-year high today at $2.1877 but fell intraday to settle in the bottom half of the range and 0.4% higher in an upside session – consistent with our bullish bias. Slow stochastics, the RSI, and candlesticks are bullish, while the MACD is neutral. We remain bullish, seeing nearby resistance at today’s high ($2.1877) and then up at $2.2000, while the 9-day ma ($2.1163) and then $2.0462 are expected to offer support. RBOB futures, where we were also bullish, added 1.9% in an upside session – consistent with our directional bias. Bulls took out the $2.2365 resistance level and now we look to $2.2820 (today’s high and a new multi-year high) and then up at $2.3000, whereas the 18-day ma ($2.1900), followed by $2.1108, are seen offering support. WTI futures edged up 0.3% in an outside session – printing a gravestone Doji star candlestick. Slow stochastics are bullish and approaching overbought territory, while the RSI and candlesticks are neutral. We are going to stick to our bullish stance for a bit longer, seeing nearby resistance at $74.25 (today’s high) and then up at $77.00, with the 9-day ma ($72.05) and $68.68 seen offering support. Finally, we awaited bullish confirmation and we received it today as NYMEX natural gas futures rose 2.3% in an upside session – hitting a fresh high of $3.383 not seen since November 2020. Slow stochastics, the RSI, the MACD, and candlesticks are all bullish and we side with the bulls now. We continue to see nearby resistance at $3.396, followed by $3.475, while $3.171 and $2.898 remain our nearby support levels.